- Replies 265

- Views 21.1k

- Created

- Last Reply

Top Posters In This Topic

-

globaldiver 51 posts

-

Spider 22 posts

-

Ani 20 posts

-

Tonge moor green jacket 17 posts

Most Popular Posts

-

How has this thread turned into a National Front rally?

-

As suspected you truly are a bit numb. So here goes. Inflation- reduces the value of everyone's money. Inflation caused (largely though not entirely) by his war. We've already touched u

-

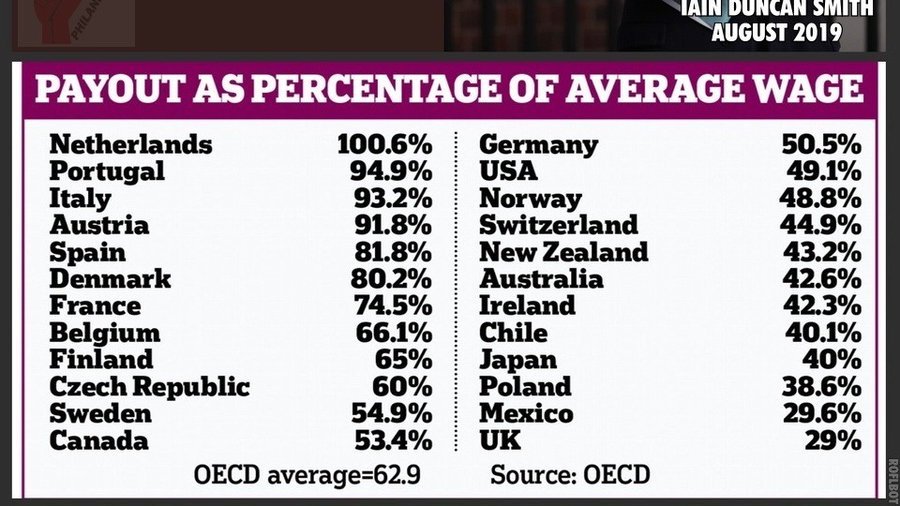

I know Imagine posting graphs with no context

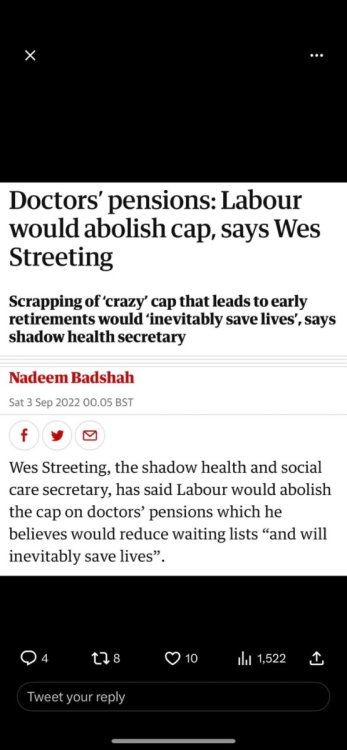

Good article

https://www.bloomberg.com/opinion/articles/2023-01-19/the-uk-beats-france-for-one-of-the-best-pensions-in-the-world?utm_source=website&utm_medium=share&utm_campaign=mobile_web_share